If you have ever felt overwhelmed by the sheer number of business loan providers online, LendingTree aims to solve exactly that problem. After spending significant time navigating the platform, I can confirm that its core promise of one application and multiple offers delivers as advertised.

LendingTree is not a direct lender. Instead, it operates as a marketplace connecting borrowers with a network of over 300 lenders spanning everything from SBA loans and traditional term loans to merchant cash advances and equipment financing.

Founded in 1996 by Doug Lebda (originally as CreditSource USA before rebranding in 1997), the Charlotte, North Carolina–based company has facilitated more than 65 million loan requests to date and is publicly traded on NASDAQ under the ticker TREE.

Throughout this review, I will walk you through exactly what the experience is like, from the first click on the homepage to receiving matched offers, and highlight where LendingTree excels and where it falls short.

What I Liked and What Gave Me Pause

Before diving into the details, here is a quick overview of where LendingTree delivers and where it can improve. I have organized these based on my experience with the platform and cross-referenced them with user reviews and expert assessments.

| PROS | CONS |

| ✓ Submit one application and receive up to five loan offers from competing lenders

✓ Free to use — LendingTree charges no fees to borrowers ✓ Extensive network of 300+ lenders covering a wide range of loan types ✓ Quick application process (under 5 minutes) with matches returned in minutes ✓ Accepts borrowers with lower credit scores than traditional banks ✓ Dedicated SMB concierge service with personalized guidance ✓ Robust educational resource center for borrowers at all stages |

✗ Not a direct lender — terms, rates, and approval depend entirely on individual partner lenders

✗ Borrowers report aggressive follow-up calls and emails from matched lenders ✗ Limited upfront information on business-specific lender partners and rates ✗ Some partner lenders may run hard credit pulls without clear authorization ✗ Rates and fees can be higher than traditional bank financing ✗ The website does not display specific APRs or loan terms until you apply |

Key Figures You Need to Know

One of the first things I noticed about LendingTree is how little concrete information the website provides before you begin the application.

Unlike some competitors that display sample rates or fee ranges upfront, LendingTree keeps its cards close until you fill out the form. That said, here is a consolidated overview of what you can expect based on the platform’s published information and my research.

| Feature | Details |

| Loan Types | SBA loans, term loans, business lines of credit, equipment financing, merchant cash advances, accounts receivable financing |

| Loan Amounts | Up to $500,000 (varies by lender) |

| Minimum Credit Score | Varies by lender; some accept as low as 500 |

| Minimum Time in Business | 12+ months (varies by lender) |

| Minimum Monthly Revenue | $8,000+ |

| Repayment Terms | 1 month to 25+ years, depending on loan type |

| Time to Funding | 1 day to 8+ weeks, depending on lender |

| Fees | No fee to use LendingTree; individual lenders may charge origination or other fees |

| Direct Lender or Marketplace | Marketplace |

Our Editorial Scoring Breakdown

I evaluated LendingTree across five core categories that matter most to business borrowers. Each score reflects a combination of hands-on testing, publicly available data, and user sentiment across platforms like Trustpilot and the Better Business Bureau.

| Category | Score | Notes |

| Online Experience | 9.5 | Learning resources, access to rates, and a mobile-friendly platform |

| Customer Service & Support | 7.5 | Multiple contact methods; some reports of aggressive outreach |

| Variety of Loan Types | 9.5 | Offers virtually all business financing types |

| Loan Amount Range | 8.0 | Up to $500,000 through partner lenders |

| Eligibility & Accessibility | 9.0 | Accepts a wide range of credit profiles |

| Overall Editorial Score | 8.7 |

Who Should Actually Use LendingTree for a Business Loan?

In my assessment, LendingTree is best suited for the business owner who does not already have a strong relationship with a bank and wants to explore multiple options without committing hours to individual applications.

If you are unsure which type of financing you even need, whether a term loan, a line of credit, or an SBA loan, LendingTree’s marketplace model can help you compare apples to apples relatively quickly.

LendingTree also works well for borrowers with less-than-perfect credit. Because the platform connects you with such a broad range of lenders, some of whom specialize in working with lower credit profiles, you are more likely to find at least one viable option than you would by approaching a single traditional bank.

That said, established businesses with excellent credit and existing banking relationships may find better rates by negotiating directly with their bank, since marketplace lenders sometimes carry higher fees to compensate for the convenience factor.

The Full Spectrum of Financing Options Available Through LendingTree

One of LendingTree’s clear competitive advantages is the sheer variety of financing products accessible through its marketplace. During my review, I found that the platform covers virtually every major category of business financing.

Here is a breakdown of what is available.

Small Business Administration (SBA) Loans

SBA loans are government-backed and typically offer the most favorable interest rates and longest repayment terms available to small businesses. Through LendingTree’s network, borrowers can access SBA 7(a) loans, CDC/504 loans, and SBA microloans. However, you will generally need a credit score of 680 or higher, at least two years in business, and strong financials. Funding can also take several weeks due to the government guarantee process.

Traditional Term Loans and Lines of Credit

For borrowers who need a lump sum with predictable monthly payments, LendingTree’s partners offer term loans with repayment periods ranging from three months to 10 years.

Business lines of credit provide more flexibility, allowing you to draw funds as needed up to a set limit and pay interest only on what you use. Both options are well-represented in the marketplace.

Equipment Financing, Merchant Cash Advances, and Invoice Factoring

LendingTree’s network also includes lenders specializing in asset-based lending. Equipment financing allows you to use the purchased equipment as collateral, which can make approval easier for businesses that might not qualify for unsecured loans.

Merchant cash advances and accounts receivable financing are also available, though borrowers should be aware that these products tend to carry significantly higher costs than traditional loans.

The company’s SMB concierge service has connected more than 5,000 borrowers with over $300 million in loans, using a consultative approach that gives business owners a comprehensive view of the options available across the lender network.

My Experience with the Application

I tested LendingTree’s business loan application process end-to-end, and I want to be transparent about what you will encounter.

You begin by selecting the type of financing you need, then answer questions about your business structure, the purpose of the loan, how much you want to borrow, how quickly you need the funds, your estimated monthly revenue, and your credit score range.

The entire process took me under four minutes. At the end, you are asked to provide your contact information: name, email, and phone number. This is the point at which LendingTree shares your details with its lending partners, and it is also where the experience can become a double-edged sword.

Within minutes of submitting my information, I received a phone call from a matched lender. Within 24 hours, I had received three additional calls and several emails. While some borrowers appreciate the speed and proactiveness, others, and I can understand this, find the volume of outreach overwhelming.

An important note: LendingTree uses a soft credit pull during the initial matching phase, which means your credit score is not affected by simply submitting the form. However, once you choose to proceed with a specific lender and formally apply for a loan, that lender will likely perform a hard credit inquiry.

SMB Concierge Service How It Works and What to Expect

One of the more recent additions to LendingTree’s business lending toolkit is its small business concierge service. Rather than simply dropping you into a pool of lender matches, the concierge model pairs you with a dedicated account executive who walks you through the available options and provides personalized recommendations based on your business profile.

According to LendingTree, this service has connected more than 5,000 borrowers with over $300 million in financing in the past year. The process works in four steps: you fill out an interest form (about two minutes), then an account executive contacts you for an introductory call, after which they provide tailored recommendations. If you decide to move forward, the same executive stays with you through the entire closing process.

I did not complete the full concierge process myself (as it requires advancing to the formal loan application stage), but the initial outreach I received was notably more structured and informative than the standard automated lender matching.

For borrowers who feel overwhelmed by choice, this added layer of human support could make a meaningful difference. It is worth noting, however, that LendingTree’s lender partners, not LendingTree itself, ultimately set all loan terms and make all approval decisions.

How Repayment Works on LendingTree

Because LendingTree is a marketplace rather than a lender, there is no single set of repayment terms to evaluate. What you will encounter depends entirely on the partner lender you choose and the type of financing you select. This is both the platform’s greatest strength and its most significant source of confusion for borrowers.

SBA loans through LendingTree’s network typically come with fixed monthly payments at competitive interest rates, with terms stretching up to 25 years for real estate loans.

Traditional term loans offer repayment windows from three months to 10 years, while lines of credit and invoice financing may have rolling repayment cycles as short as one month. Merchant cash advances use a factor rate model, meaning you repay a fixed percentage of your future sales rather than a traditional interest rate.

Online reviews suggest that some loan types accessible through LendingTree may carry prepayment penalties. I strongly recommend asking each matched lender about early repayment terms before signing any agreement. Most loans are set up for automatic payments from your business bank account, so ensure you are comfortable with the withdrawal schedule before committing.

Can You Trust LendingTree?

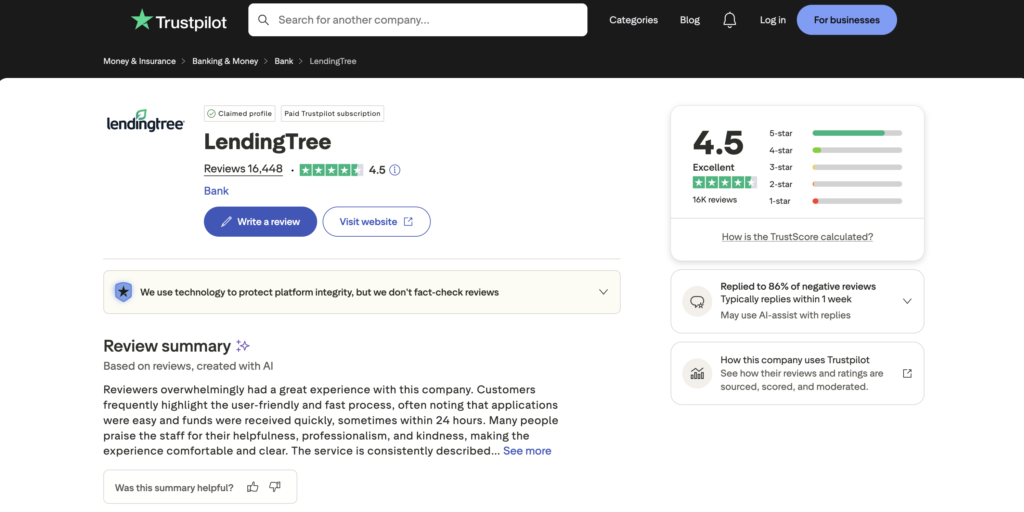

LendingTree’s public reputation tells two somewhat different stories depending on where you look. On Trustpilot, the company holds a 4.5 out of 5 rating with over 16,000 reviews — a strong score by any measure. The Better Business Bureau has accredited LendingTree since 2019 and awarded it an A+ organizational rating. However, the BBB’s customer review score sits at just 1.05 out of 5 based on approximately 111 reviews, a stark contrast that warrants attention.

Positive reviews consistently praise LendingTree’s speed and simplicity. Users appreciate the ability to compare multiple offers without visiting individual lender websites, and many report securing funding within days of their initial application. Several reviewers specifically highlight the platform’s usefulness for refinancing existing loans at better rates.

Negative reviews, however, cluster around a few recurring complaints. The most common concern is the volume of unsolicited contact from matched lenders. Some borrowers report receiving multiple phone calls daily, even after requesting to stop.

Others express frustration with lenders performing hard credit pulls that they did not feel they had authorized. There are also complaints about the gap between advertised rates and the rates borrowers actually received upon full application. One recent BBB complaint from March 2026 alleged that a LendingTree business loan advisor misrepresented the nature of the credit inquiry process.

It is important to note that many reviews across both platforms cover LendingTree’s consumer products (mortgages, personal loans) rather than business loans specifically. Still, the feedback patterns are consistent enough to suggest that the outreach volume issue is systemic rather than isolated to one product line.

What to Expect When You Need Help

LendingTree offers customer support through a toll-free phone number (800-813-4620) and an email contact form on its website. Phone support is available Monday through Thursday from 8:00 AM to 9:00 PM, Fridays from 8:00 AM to 8:00 PM, and Saturdays from 10:00 AM to 7:00 PM Eastern Time. There is no Sunday support or live chat option, which is a notable omission for a company of this scale.

In my experience, the phone support team was professional and able to answer general questions about how the marketplace works. However, because LendingTree does not originate loans, the support team redirected more specific questions about loan terms and rates to the individual partner lenders, which is expected but can feel circular when you are trying to compare options at a high level before committing to a specific lender.

The website also hosts an extensive educational resource center with articles, videos, and guides covering topics ranging from the basics of business financing to best practices for debt management. I found the educational content genuinely useful, particularly the lender comparison pages and the small business loan calculator.

The FAQ section, however, is not as easy to navigate as it could be, and finding answers to very specific questions often requires digging through multiple pages.

How LendingTree Stacks Up Against Other Business Loan Marketplaces

LendingTree is not the only lending marketplace available to small business owners, and understanding where it sits in the competitive landscape is important for making an informed decision.

Lendio, for example, works with over 75 lenders and offers startup loans with terms of up to 25 years. It holds a 4.7 out of 5 Trustpilot rating with over 21,000 reviews and is known for a more hands-on matching process.

Fundera (now part of NerdWallet) offers a similar marketplace model with strong editorial content and educational resources. Biz2Credit, meanwhile, positions itself as more of a hybrid — it operates as both a marketplace and a direct lender, offering revenue-based financing, term loans, and commercial real estate loans with 24-hour approval decisions.

Where LendingTree distinguishes itself is in sheer scale and brand recognition. With over 300 lenders in its network and nearly three decades of operating history, it offers one of the broadest pools of potential matches available anywhere. The tradeoff is less hands-on curation than some competitors provide, and the aggressive lender outreach that comes with distributing your information across a large network.

Should You Use LendingTree for Your Next Business Loan?

After thoroughly testing the platform, reviewing user feedback, and analyzing the competitive landscape, I believe LendingTree earns its place as a useful starting point for many small business borrowers, but with important caveats.

The platform excels at what it was designed to do: simplify the comparison process, surface multiple loan options quickly, and give borrowers leverage by making lenders compete.

The application is fast, the lender network is massive, and the zero-cost model means there is no financial risk in exploring your options. The addition of the SMB concierge service addresses a real need for borrowers who want human guidance rather than just an automated feed of matches.

The downsides are real but manageable. You will need a tolerance for lender outreach, and you should go in understanding that the rates and terms you see will depend entirely on the partner lenders you are matched with, not on LendingTree itself. Read every disclosure carefully, confirm whether credit inquiries will be soft or hard before proceeding with any lender, and do not hesitate to compare LendingTree’s matches against quotes from your existing bank.

For business owners who are early in their search, uncertain about what type of financing they need, or working with imperfect credit, LendingTree offers genuine value. For those with established banking relationships and strong credit profiles, it is worth using as a benchmark even if you ultimately finance elsewhere.